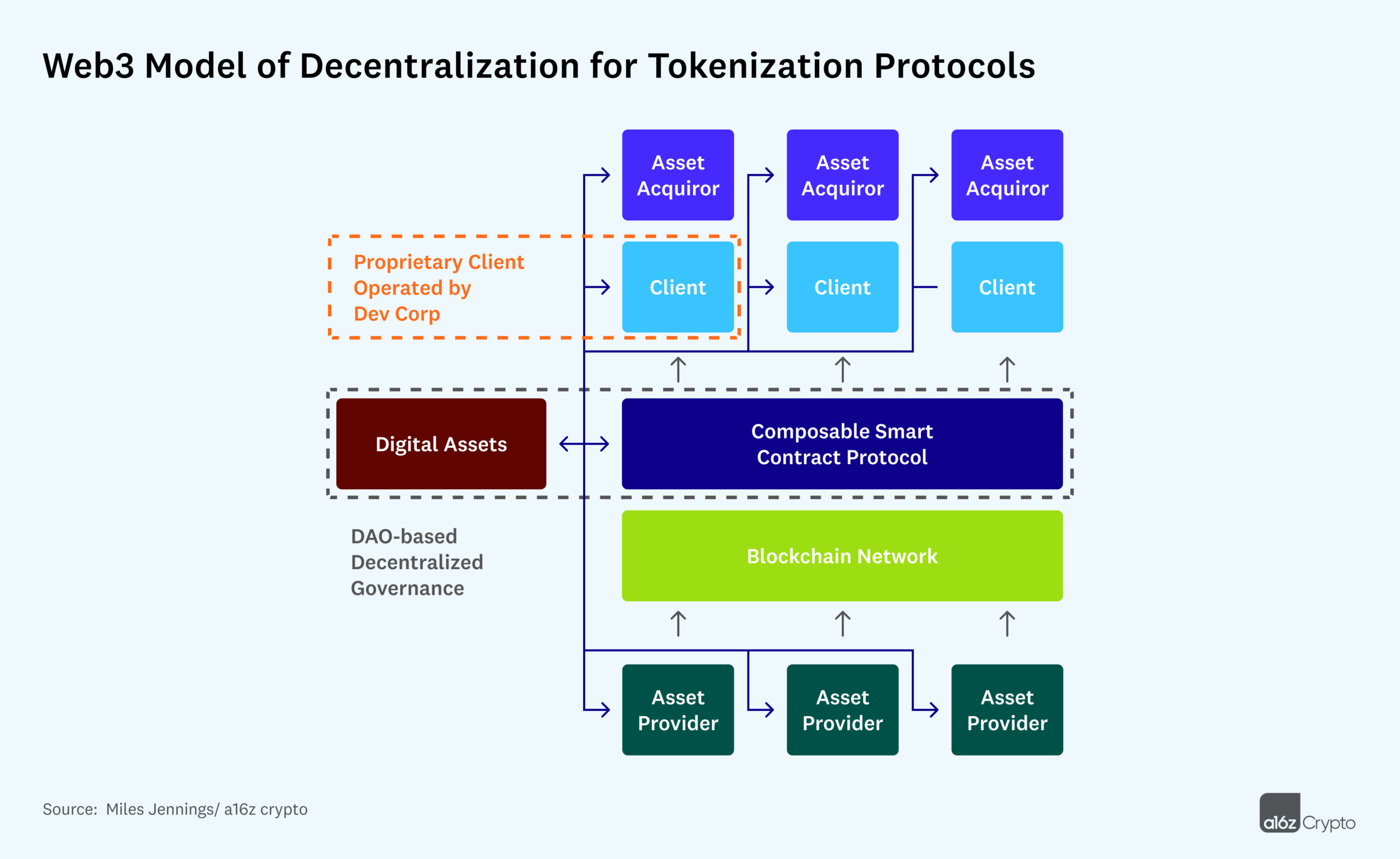

Tokenization protocols are another type of emerging web3 system. In these systems, assets are onboarded to a blockchain, tokenized by a smart contract protocol, and then sold or used for other purposes. Types of tokenization protocols include serial NFT-minting projects, digital asset marketplaces, and protocols that tokenize real-world assets.

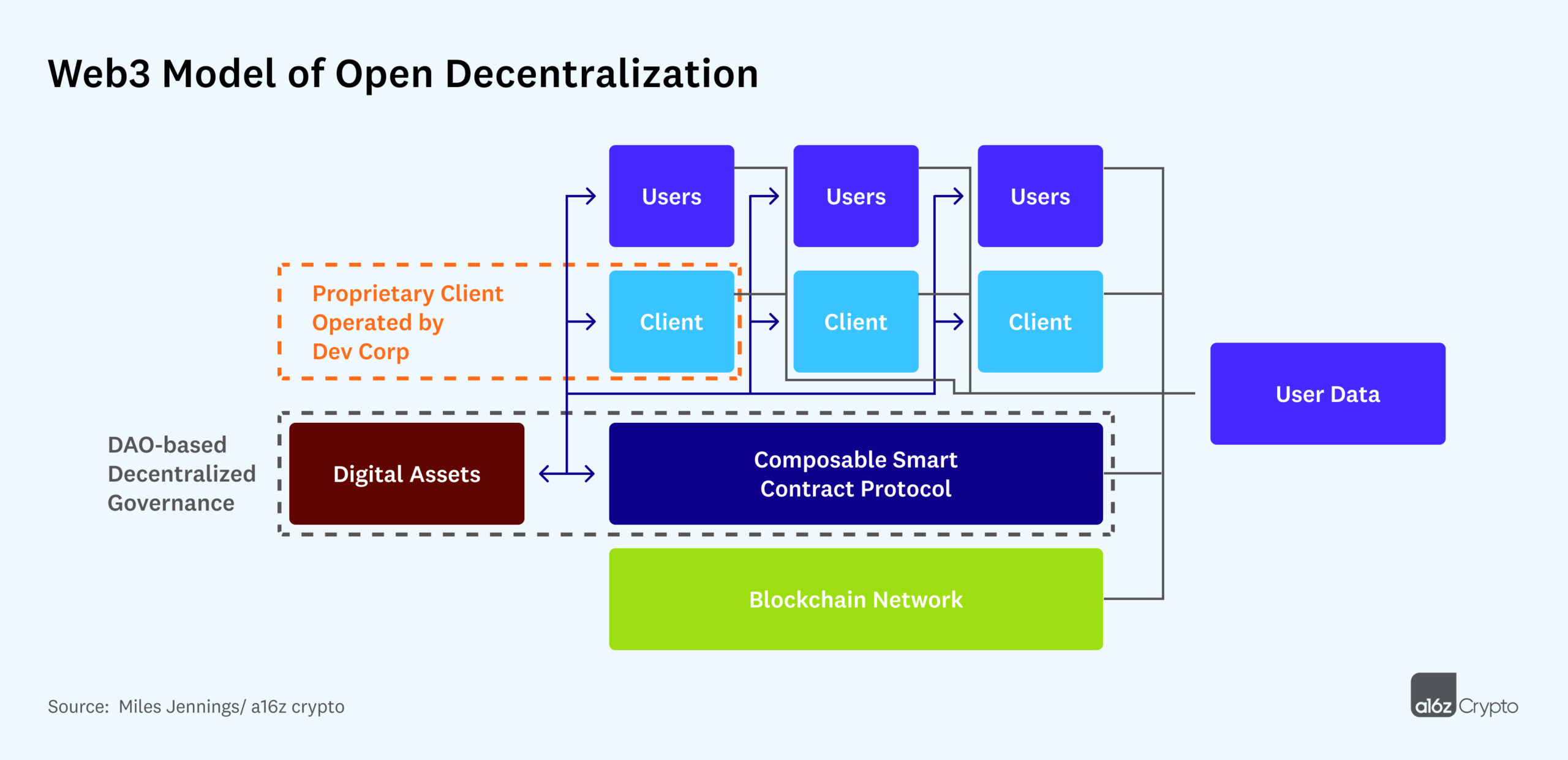

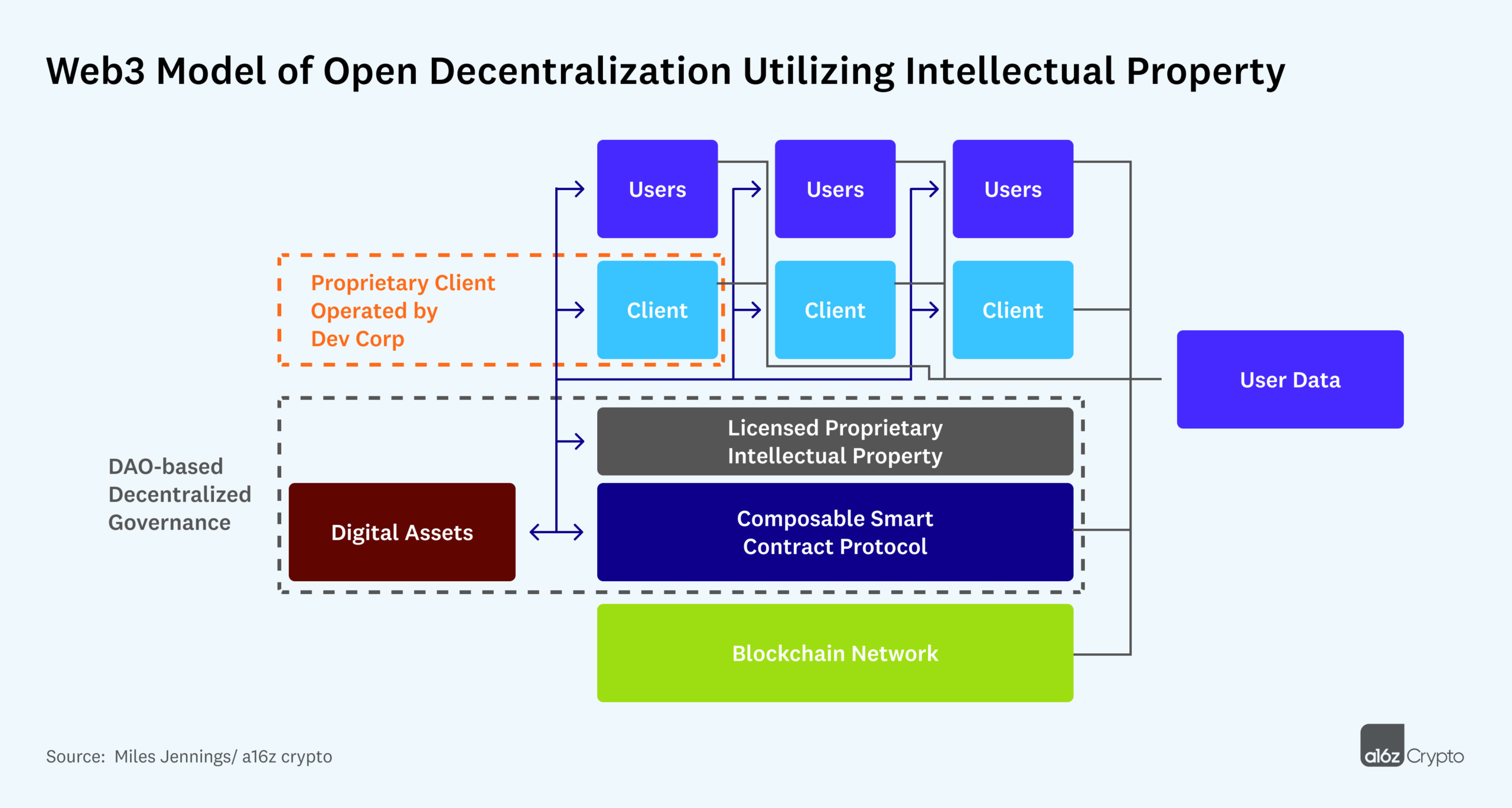

The open decentralization model below reflects:

- assets brought on-chain from multiple providers through a shared smart contract protocol;

- the smart contract protocol tokenizing such assets;

- the sale or use of such tokenized assets through multiple clients;

- native digital asset distributions and incentivization mechanisms; and

- the launching of DAO governance with respect to the community intellectual property and DAO treasury.

In this model, economic decentralization is achieved through sufficient diversity of inputs (asset providers) and outputs (asset acquirors), as well as the decentralization of the layers through which the tokenized assets flow (the blockchain, the smart contracts, and the clients).

The protocol’s DAO could also use explicit incentives (fungible token awards, no commissions/ fees, etc.) to:

- incentivize asset providers to provide assets to the system;

- incentivize clients to make a market in the tokenized assets; and

- incentivize acquirors to acquire such assets or to consume them.

While the initial developer company may initially play a significant part in any of these roles (asset provider, client operator, asset acquiror), once the system is decentralized, the developer company would eventually be just one of many actors in any given role. This would limit the risk of any significant information asymmetries accruing to it and reduce the reliance on its managerial efforts. In addition, many roles could be undertaken by the DAO and/ or subDAOs.

Over time, the explicit incentives could also be adjusted to account for potential shortfalls on either the supply side or the demand side. In a decentralized marketplace for instance, token incentives to sellers (the supply side) could be increased to bring more goods for sale onto the platform; and token incentives to buyers (the demand side) could be increased to encourage more purchases.

From a legal decentralization perspective, the key questions, yet again, would be: Are the essential managerial efforts of any third party necessary to drive the success or failure of the web3 system? And would there be the potential for significant information asymmetries to arise? The answer to both questions depends on whether the DAO could effectively manage its incentives to balance supply and demand as in the example above — but more broadly, it’s really about preventing any single asset provider, asset acquiror, or client from becoming so important that the success of the entire system relies on any one entity’s efforts.

For additional models and use cases, as well as more details relating to the above models, please see the full paper.

* * *

Builders of web3 systems currently face numerous challenges in initiating, managing, and scaling decentralization. But the framing of decentralization as a single design challenge with three aspects — technical, economic, and legal — should provide a strong reference guide to help builders as they use the novel components of web3 systems to overcome these challenges, even as regulatory requirements may shift.

Failure to account for all three of these elements will lead us to a web3 that falls short of the future that blockchain technology and cryptocurrencies make possible. No one wants a “web3“ that’s built on new tech, but that is otherwise indistinguishable from web2. Instead, by building systems that carefully and deliberately design for decentralization, builders can create digital infrastructure, and give life to decentralized economies, which will form the foundation of the internet for decades to come. It’s time to build that internet, and that future.

Special thanks to Chris Dixon, Sriram Krishnan, Sonal Chokshi, Eddy Lazzarin, David Kerr, and Adam Zuckerman for their contributions and insights, as well as to all of the authors of the works I reference in the more comprehensive version of this piece.

***

The views expressed here are those of the individual AH Capital Management, L.L.C. (“a16z”) personnel quoted and are not the views of a16z or its affiliates. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by a16z. While taken from sources believed to be reliable, a16z has not independently verified such information and makes no representations about the current or enduring accuracy of the information or its appropriateness for a given situation. In addition, this content may include third-party advertisements; a16z has not reviewed such advertisements and does not endorse any advertising content contained therein.

This content is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. You should consult your own advisers as to those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Furthermore, this content is not directed at nor intended for use by any investors or prospective investors, and may not under any circumstances be relied upon when making a decision to invest in any fund managed by a16z. (An offering to invest in an a16z fund will be made only by the private placement memorandum, subscription agreement, and other relevant documentation of any such fund and should be read in their entirety.) Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Andreessen Horowitz (excluding investments for which the issuer has not provided permission for a16z to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://a16z.com/investments/.

Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Please see https://a16z.com/disclosures for additional important information.